Business Valuation Guide

Discounted Cash Flow

This key income-based valuation method in ValuAdder requires the following inputs:

- Net cash flow projections

- Discount rate

- Terminal value or future business sale gain value

For the purposes of the Discounted Cash Flow business valuation, the net cash flow is what the owners can remove from the business without impairing its operation. Assuming that both debt and equity acquisition capital is used, the net cash flow is calculated as follows:

- Net after-tax income.

- Plus depreciation and amortization expenses.

- Plus the after-tax portion of the interest expense.

- Minus capital expenditures. Historic requirements can be found on the company’s Statements of Cash Flows.

- Minus increases in working capital.

Step 1: Forecast your business cash flows

Establish your business net cash flow projections over the required period, e.g. 5 years into the future. At the end of this period, if a business sale is planned, estimate the gain from the business sale. If you plan to keep operating the business beyond this point, capitalize the expected cash flow to determine the so-called terminal value.

Step 2: Calculate your discount rate

To estimate the discount rate, consult the How to build up the equity discount rate Guide and the WACC definition.

Step 3: Estimate your business terminal value

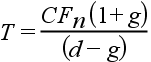

The terminal value can be computed using the following formula:

Where CFn is the cash flow expected to be received in year n, d is the discount rate, and g is the expected average annual growth rate in the cash flow. The difference between the discount rate and the expected average cash flow growth rate in the denominator above is the capitalization rate.

Example

Assume that the business net cash flow will be $150,000 in year 5. Assume further that the cash flow can be expected to grow annually at the rate of 5% going forward. If your discount rate is 25%, then the terminal value is:

The capitalization rate in this case is 20%, which is the difference between the discount rate of 25% and the expected average growth rate of 5%.

Please note that your choice of the capitalization rate is significant when determining the terminal value. The above example indicates that the business value is 787,500/150,000 or 5.25 times its net cash flow in year 5.