Business Valuation Glossary

Weighted Average Cost of Capital

Definition

The total cost of the capital used to finance or purchase a business. It is computed from the respective costs of debt and equity and their relative proportion in the deal structure.

What It Means

The weighted average cost of capital (WACC) reflects the overall costs of combined debt and equity capital used to finance business operations or acquisition. It is the basis of determining the discount rate for the Discounted Cash Flow (DCF) business valuation method.

For example, let’s assume that the buyer purchases a business with 50% cash down payment (equity) and the balance (debt) being financed by the seller. Let’s say that the buyer’s downpayment costs 30% per year, the seller’s note carries an 8% annual interest, and the business tax rate is 30%. Then the weighted average cost of the capital used to purchase the business is:

In typical business valuation and acquisition scenarios, the WACC can be computed using the general formula:

![WACC = [ke × E] + [kn × (1 − t) × N] + [kl × (1 − t) × L]](https://cdn.valuadder.com/glossary/WACC-formula.png?hash=2j6wqgczgl)

Where ke is the discount rate representing the cost of equity capital such as the business buyer down payment, E is the percentage of down payment in the total deal structure, kn is the pretax interest on the seller’s note, N is the seller’s note percentage, t is the business tax rate, kl is the bank loan interest and L is the percentage of the bank loan used to finance the business purchase. Note that the sum of E, N and L always equals 100%.

Book value versus market value of equity

As the formula demonstrates, to calculate the WACC, you need to estimate the values of all equity and debt components in the deal structure.

Importantly, in business valuation situations, the calculation requires the market value of equity, rather than its book value. This requirement leads to the following iterative procedure for estimating WACC:

Calculating WACC by iteration

- Estimate the market value of all debt such as the seller’s note and bank loan.

- Project future business net cash flow (NCF), e.g. for 3–5 years.

- Estimate the average annual growth rate in the net cash flow.

- Use the WACC formula and the book value of business equity to calculate the initial estimate of WACC.

- Estimate the market value of equity using the WACC initial estimate, first year NCF projection and the average NCF growth rate from above.

- Re-calculate the WACC using the new equity value estimate while keeping the debt values constant.

- Iteratively adjust the initial WACC input until it approximates the calculated WACC result.

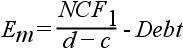

You can use the following constant growth capitalization model to estimate the market value of business equity when calculating the WACC:

Where Em is the market value of business equity, NCF1 is the net cash flow projection in the first year following your business valuation, d is the discount rate you are estimating with this iterative procedure, and c is the average annual growth rate in the projected business net cash flow.

Example

You would like to estimate the discount rate as the WACC in order to determine the value of the privately held XYZ, Inc for potential acquisition. The company parameters are as follows:

- Book value of equity is $700,000.

- Seller is prepared to carry a note of $700,000 at 8.25% annual interest.

- ABC Bank has offered to finance part of the purchase price with a loan of $100,000 at 9.25% annual interest.

- The company tax rate is 40%.

- The equity discount rate is 35%.

- You project the first year net cash flow to be $80,000.

- You expect net cash flow to grow at 7.73% on average.

Step 1: Estimate the WACC using book value of business equity

| Type of Capital | Amount | % of Total | Cost, pretax | Cost, after-tax | Weighted Cost |

|---|---|---|---|---|---|

| Equity, book value | $700,000 | 63.64 | 35% | 35% | 22.27% |

| Seller’s note | $300,000 | 27.27 | 8.25% | 4.95% | 1.35% |

| Bank loan | $100,000 | 9.09 | 9.25% | 5.55% | 0.5% |

| WACC, first estimate: | 24.13% | ||||

Step 2: Calculate the WACC using the market value of equity

In this step, you use the WACC estimate from Step 1 to calculate the market value of business equity using the constant growth capitalization formula. The values of seller’s note and bank loan are the same. Calculating the new WACC, you get:

| Type of Capital | Amount | % of Total | Cost, pretax | Cost, after-tax | Weighted Cost |

|---|---|---|---|---|---|

| Equity, market value | $87,819 | 18 | 35% | 35% | 6.3% |

| Seller’s note | $300,000 | 61.5 | 8.25% | 4.95% | 3.04% |

| Bank loan | $100,000 | 20.5 | 9.25% | 5.55% | 1.14% |

| WACC, second estimate: | 10.48% | ||||

Step 3: Iterating to find the actual WACC value

Notice that there is quite a difference between the WACC estimates in Step 1 and 2. The actual value lies somewhere in between. You can adjust your initial WACC estimate in step one and re-calculate your WACC result until the two values equal each other. In this example, this value is 18.66%. Your final capital structure and costs look as follows:

| Type of Capital | Amount | % of Total | Cost, pretax | Cost, after-tax | Weighted Cost |

|---|---|---|---|---|---|

| Equity, market value | $331,962 | 45.35 | 35% | 35% | 15.87% |

| Seller’s note | $300,000 | 40.99 | 8.25% | 4.95% | 2.03% |

| Bank loan | $100,000 | 13.66 | 9.25% | 5.55% | 0.76% |

| WACC, final estimate: | 18.66% | ||||